Airtel is shutting down its music streaming service, Wynk Music, and absorbing its employees. This decision aligns with Airtel’s new partnership with Apple to offer Apple Music to iPhone users. Despite earlier efforts to monetize Wynk

Airtel is shutting down its music streaming service, Wynk Music, and absorbing its employees. This decision aligns with Airtel’s new partnership with Apple to offer Apple Music to iPhone users. Despite earlier efforts to monetize Wynk

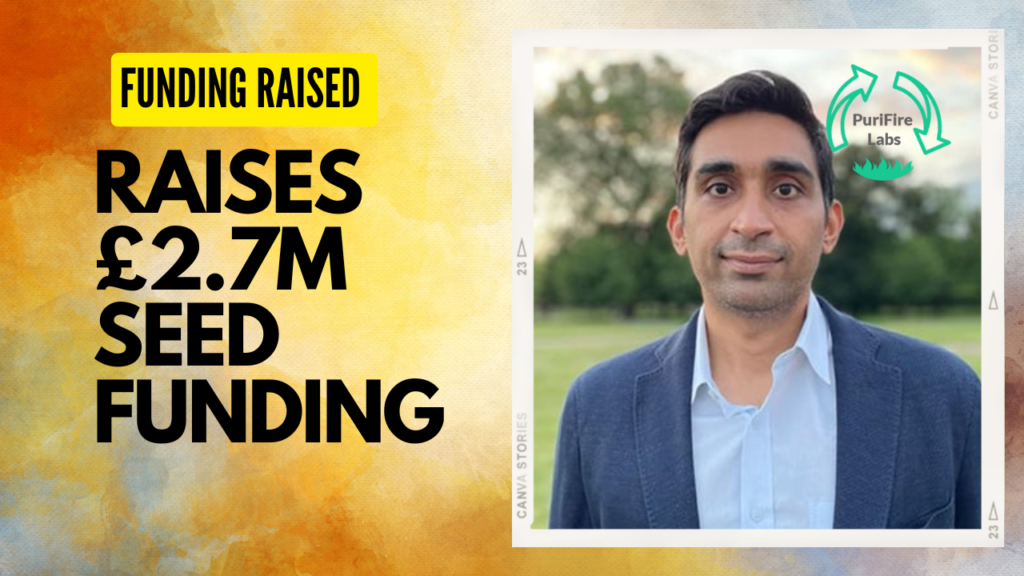

Cambridge-based PuriFire secured £2.7M in Seed funding led by HICO Investment Group, with plans to launch a pilot project by mid-2025. The startup, founded by Dr. Matthew Pearce and CEO Neel Shah, focuses on sustainable green hydrogen and methanol solutions to support a low-carbon economy.

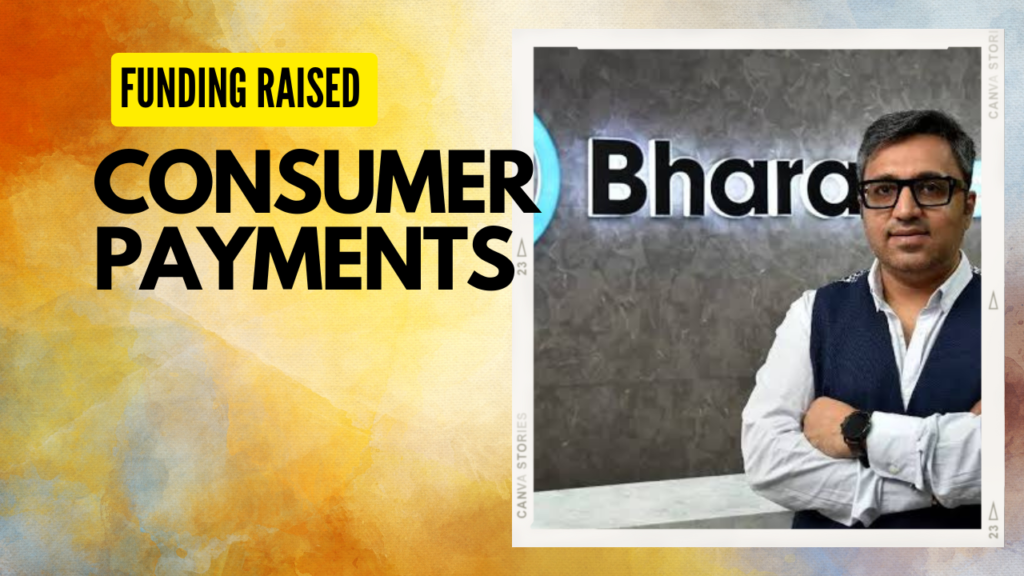

BharatPe has rebranded its postpe app, entering the consumer payments space to compete with PhonePe, Google Pay, and Paytm. The new BharatPe app allows UPI payments, bill payments, and features UPI Lite for quick transactions. BharatPe aims to challenge the market leaders in the growing UPI ecosystem.

Proptech firm Square Yards reported a 52% increase in revenue for Q1 FY25, reaching Rs 261 crore with a gross transaction value of Rs 10,053 crore. Despite growth, the company posted a negative EBITDA margin of Rs 32 crore. Square Yards aims for Rs 1,506 crore revenue in FY25.

Health-tech startup Sunfox Technologies raised Rs 15 crore in a pre-Series A round led by Venture Catalysts. The funds will be used for global expansion and scaling its portable ECG device, Spandan. Co-founded in 2016, Sunfox’s innovative technology has saved over 10,000 lives across 20 countries.

Amazon plans to enter India’s quick commerce market in early 2025, challenging leaders BlinkIt, Zepto, and Swiggy Instamart. Nishant Sardana will lead this new vertical. The move follows Amazon’s competitor Flipkart’s entry into the sector and Tata’s BigBasket pivoting to quick deliveries.

Post-sales service firm Servify raised Rs 84 crore ($10 million) in a Series D tranche from Bajaj Holdings, Trifecta, and Innoven Capital. The funding mix includes equity and debt, valuing the Mumbai-based company at Rs 7,074 crore ($852 million). Servify continues to grow, despite net losses.

Insurtech startup InsurancePadosi raised $500K in a pre-seed round led by Antler. The funds will enhance technology, expand product offerings, and boost sales and marketing. Founded in 2023, the platform offers AI-driven personalized insurance recommendations and aims to educate 200,000 individuals about insurance needs within the next year.

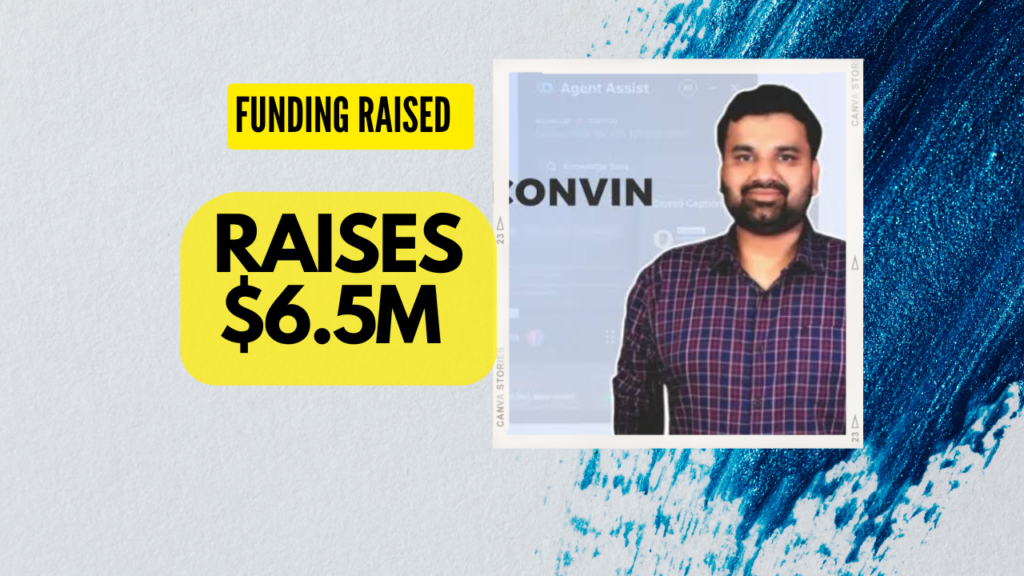

Conversation intelligence platform Convin secured $6.5 million in Series A funding led by India Quotient, with support from JSW Ventures and others. Founded in 2021, Convin uses AI to enhance customer-facing teams’ efficiency. The funds will help expand the team and distribution channels as the company projects significant growth.

Spiritual tech startup My Tirth India is closing down due to a funding shortfall, following the death of its primary investor, Subrata Roy. Despite the sector’s growth, with $40 million raised by competitors, My Tirth India couldn’t sustain operations. The startup had focused on facilitating pilgrimages across India.